General Liability

While third-party partnerships are essential for any project, they also carry inherent risks—making it important for all parties involved to have active liability policies in place.

What is Commercial General Liability?

Commercial general liability (CGL) insurance protects a business if it gets sued; this insurance can cover claims for both bodily injury and property damage. In other words, commercial general liability protects your businesses in the event of a lawsuit. Also known as CGL insurance, liability insurance, or general liability insurance, this type of coverage is the first line of defense in the event of a loss. In fact, is the broadest in types of incidents it protects a company against.

What does CGL insurance cover?

As one of the broadest types of insurance, it covers:

- Bodily Injury & Property Damage

- Advertising & Personal Injury

- Medical Payments Coverage

General Liability Examples:

For example, say a hotel chain hires a contractor to install a pool in one of its locations. One of the subcontractors leaves equipment out, and a hotel staff member trips and falls—spraining her ankle, and breaking a window while trying to catch herself. (Ouch.)

For example, say a hotel chain hires a contractor to install a pool in one of its locations. One of the subcontractors leaves equipment out, and a hotel staff member trips and falls—spraining her ankle, and breaking a window while trying to catch herself. (Ouch.)

While CGL won’t cover her injury, it will cover any lawsuits she might place on the contractor, as a result.

If those in the previous example wanted to extend their coverage to include property damage (the broken window), they might add property liability insurance to the CGL policy—covering charges for damages you’re legally responsible for.

Personalizing your CGL policy to your unique needs as much as possible helps mitigate risks and ensure continuous coverage.

Policy Limits

CGL policies also contain limits for how much the insurer will cover for specific events.

These include:

- Each Occurrence: Total an insurer will pay each time a claim occurs

- Damaged to Rented Premises: Funds available if policyholder damages the space they are renting

- Medical Expense Limits: Amounts paid for reasonable medical injury caused by an accident, applying separately to each injured person

- Personal & Advertising Injury: Covers false arrest, detention, and imprisonment, and advertising injuries such as slander, libel, and invasion of privacy

- General Aggregate: Total amount a policy is obligated to pay in a single term. It can respond in three ways: per policy, per project, and per location.

- Per Policy: The maximum amount an insurer will pay for the total of all claims covered by an insurance policy

- Per Project: Limits applying to each project of the policyholder (commonly used by owners of buildings and retail stores)

- Per Location: Limits applying to each location of the policyholder (commonly used by companies and contractors doing project work, such as in construction trades)

- Products-Completed Operations: Protects business against claims of injury or property damage occurring after work has been completed, resulting from a product made or sold by your company

CGL Coverage Types

Within CGL insurance, there are two main types of coverage: occurrence and claims-made.

- Occurrence: Protects a business from any covered incident during the policy period, regardless of when the claim is reported.

- Claims-Made: Covers claims that occur and are reported within the policy period.

How to Renew Your CGL Insurance

- Gather all pertinent information (such as payroll costs, certificates of insurance, and address changes).

- Perform a risk assessment.

- Assess previous renewals.

- Compare rates and policies from your insurer and others.

- Renew your current policy or purchase a new one.

You’ll want to begin this process two to three months before the policy expires. Wait any longer, and you may be subject to accepting more expensive, inadequate coverage to prevent gaps.

Umbrella Insurance & Excess Insurance

While umbrella and excess insurance both increase insurance policy limits, there are several key differences between the two.

What Is Excess Insurance?

Excess insurance does not expand policy terms, but covers higher financial limits in case of unforeseen, catastrophic claims or loss.

What Is Umbrella Insurance?

Umbrella insurance is a form of excess insurance. It does expand the policy terms, and also provides broader coverage to encompass losses not outlined in the policy.

Liabilities exceeding the policy scope become the policyholder’s responsibility, not the insurer. So, excess and umbrella insurance kick in when we’ve exhausted a commercial general liability, auto liability, or any other policy it sits on top of.

For instance, if Terrence Traveler is visiting another country, his umbrella policy may cover auto liability in that area, even if his commercial auto policy doesn’t include coverage for these territories.

For instance, if Terrence Traveler is visiting another country, his umbrella policy may cover auto liability in that area, even if his commercial auto policy doesn’t include coverage for these territories.

However, if he gets into an accident using a rental car while traveling, and tries to add excess or umbrella insurance after the fact, it may not be covered.

The best way to ensure continuous coverage is to purchase these insurance addendums with your car insurance.

Workers’ Compensation & Employers’ Liability

Workers’ compensation, or workman’s comp, pays for expenses resulting from workplace injuries, including medical care, lost wages, and rehabilitation. If a worker dies from the injury, it may also cover their funeral expenses.

Workers’ comp doesn’t cover claims of:

- Gross Negligence

- Discrimination

- Malicious Intent

- Wrongful Termination

- Failure to Promote

- Intentional Injury

- Emotional Injury

- Injuries From Fights Caused by Employees

- Injuries Occurring During Commute or Intoxication

Let’s consider an example:

![]() If a contracted painter falls off a ladder and breaks an arm, workers’ compensation would potentially pay for their medical bills, paid leave, and other rehabilitative costs.

If a contracted painter falls off a ladder and breaks an arm, workers’ compensation would potentially pay for their medical bills, paid leave, and other rehabilitative costs.

In this same example, if the painter was using a ladder provided by the business owner and decided to sue them, workers’ comp may also cover the painter’s legal expenses.

But what about the business owner?

This is where employers’ liability insurance comes in.

It’s an employer’s legal responsibility to pay for damages resulting from work-related injury for full-time employees. However, some exemptions apply for:

- Casual Workers

- Employees Working on Commission

- Family Members

- Part-Time Workers

- Farmhands

- Real Estate Agents

- Insurance Agents

- Business Owners

In the United States, most states are required to provide some form of workers’ compensation, and employers are responsible to pay premiums.

So, employers’ liability insurance helps offset these costs by covering lawsuits that may result from an employee injury or illness.

The difference between these two policies is: workers’ comp covers employees, whereas employers’ liability covers employers.

Riggers Liability

Riggers liability covers a contractor's liability from moving others’ property or equipment, while under the care of a rigging contractor.

![]() For example, let’s say a rigging contractor was moving a piece of equipment with a crane, but dropped and damaged the equipment due to improper rigging. The contractor’s riggers liability insurance would kick in to cover the costs of the damaged equipment itself.

For example, let’s say a rigging contractor was moving a piece of equipment with a crane, but dropped and damaged the equipment due to improper rigging. The contractor’s riggers liability insurance would kick in to cover the costs of the damaged equipment itself.

Garage Liability Insurance

Garage liability insurance insures bodily injury or property damage to a vehicle while under the care of the insured business.

Automotive dealerships, repair shops, parking garages, tow-truck operators, service stations, and others in the automotive industry often purchase this type of umbrella insurance as an addition to their business liability coverage.

If a parking garage wall collapses, for instance, the property manager’s garage liability insurance will cover any bodily injury or property damages to vehicles in the vicinity.

If a parking garage wall collapses, for instance, the property manager’s garage liability insurance will cover any bodily injury or property damages to vehicles in the vicinity.

Evidence of Property Coverage

Appropriately dubbed evidence of property coverage,the ACORD 28 and 27 forms prove your property is covered and protected under an insurance policy.

These standardized forms prove to be useful when interacting with parties who have a direct interest in the insured property, thereby serving as a critical component in the property insurance processes.

Inland Marine Insurance

What Is Inland Marine Insurance?

Inland marine and cargo insurance are both types of property insurance covering goods, materials, and other items in transit. While they have similar elements, there are some key differences between the two.

What Does Inland Marine Insurance Cover?

Inland marine insurance typically covers property while transported via land or waterways. It may be purchased as an add-on to an existing business insurance policy or as a separate policy.

Inland marine coverage can repair or replace items if damaged by fire, wind, theft, water damage, and hail.

If a shipping vessel encounters a storm and its load is tossed into the sea, for example, inland marine insurance may cover the costs of the lost shipments.

If a shipping vessel encounters a storm and its load is tossed into the sea, for example, inland marine insurance may cover the costs of the lost shipments.

Cargo Insurance

Cargo insurance is a form of transport insurance that protects goods while in transit.

It is especially beneficial to independent truckers, who are responsible for their cargo during transport and may not have access to traditional corporate protection.

For example, if a truck carrying packages of merchandise is broken into, and some of the packages are stolen or damaged, the policyholder’s cargo insurance would cover costs of the damage.

For example, if a truck carrying packages of merchandise is broken into, and some of the packages are stolen or damaged, the policyholder’s cargo insurance would cover costs of the damage.

Insurance Endorsements

Insurance endorsements, also referred to as “riders,” are additional documents that modify an existing policy.

They can add or limit coverage not otherwise specified, and provide a more detailed explanation of certain elements within the policy such as coverage, deductible amounts, or excluded items.

![]() For example, if you wanted to add coverage for floods or earthquakes to a homeowner’s insurance policy, you would need an endorsement outlining those areas of coverage.

For example, if you wanted to add coverage for floods or earthquakes to a homeowner’s insurance policy, you would need an endorsement outlining those areas of coverage.

While a handful are standardized, many endorsements are drafted to meet the specific concerns and underwriting needs of an insurer—creating important differences regarding who is covered, when, and to what extent.

There are also different versions of insurance endorsements, including:

- Standard Endorsements: Modify names, addresses, coverage, and other aspects insureds commonly change about their policy, using a template provided by the insurer

- Non-Standard Endorsements: Typically involve insurers making changes to the template or drafting new documents

- Mandatory Endorsements: Refer to those required by law, such as flood insurance in a flood zone

- Voluntary Endorsements: Not required by law. Most endorsements fall under this category, such as earthquake insurance.

![]() For instance, if a subcontractor is hired to lay tile in a kitchen remodel, they can designate a general contractor they’re working for as an additional insured in their insurance policy. This ensures if the subcontractor runs into any work-related lawsuits, the general contractor can protect itself under the subcontractor’s policy.

For instance, if a subcontractor is hired to lay tile in a kitchen remodel, they can designate a general contractor they’re working for as an additional insured in their insurance policy. This ensures if the subcontractor runs into any work-related lawsuits, the general contractor can protect itself under the subcontractor’s policy.

In the previous example, we mentioned the term “additional insured.” This is one of a few most commonly requested insurance endorsements, along with primary and non-contributory endorsements.

Let’s review both in more detail.

Endorsement Form Anatomy

Reading and identifying different endorsement forms can be confusing. While there are a lot of standardized endorsements forms, there are also insurance endorsements written to meet specific concerns and underwriting needs for different companies and projects. It is important to familiarize yourself with these different types of forms so you know who is covered, how and when they are covered, and the conditions by which coverage is to be provided. For example, there are many different additional insured endorsement forms.

The different versions of insurance endorsements, include:

- Standard Endorsements: Modify names, addresses, coverage, and other aspects insureds commonly change about their policy, using a template provided by the insurer

- Non-Standard Endorsements: Typically involve insurers making changes to the template or drafting new documents

- Mandatory Endorsements: Refer to those required by law, such as flood insurance in a flood zone

- Voluntary Endorsements: Not required by law. Most endorsements fall under this category, such as earthquake insurance.

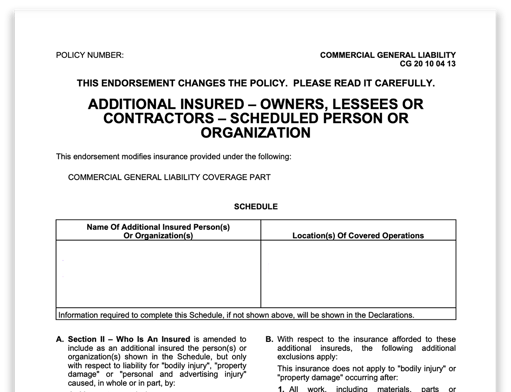

ISO Standardized Endorsement Forms

An ISO form is a type of insurance policy endorsement written by the Insurance Services Office (ISO) that is so commonly used it has become an industry standard.The beauty of this type of standardization is the ability to quickly recognize which endorsement you are dealing with.

Let’s take a closer look at the different aspects of a standard additional insured form, the Insurance Services Office (ISO) Scheduled Person or Organization (CG 20 10).

- Number of the Policy Being Endorsed: This must match the policy number listed on the COI.

- Endorsement Number: Each endorsement number indicates its identifying information. The first two digits denote policy type, while the next four digits delineate both the endorsement category within the coverage type and the specific endorsement.

Let’s continue using our CG 20 10 04 13 endorsement as an example:

- i.“CG” identifies the endorsement as commercial general liability.

- ii.The first number, “20,” signifies the category is additionally insured.

- iii.The second number, “10,” means it is for scheduled ongoing operations.

- iv.The last four digits refer to the month and year it was put into use. “04 13” indicates this document was implemented in April 2013.

Additional Insureds

What Are Additional Insureds?

Additional insureds are people or entities coverage has been extended to in the event of a claim or negligent acts. Additional insureds usually have some degree of liability because of their relationship to the named insured.

However, they are not responsible for paying premiums, receiving notices of cancellation, or negotiating policy terms.

![]() For example, let’s say a bakery hires a general contractor to install a new roof, and has its contractors list it as an additional insured. During construction, debris falls and injures a bakery employee. Out of work for six weeks, they sue the contractor, who, named as an additional insured, is covered by the subcontractor’s policy.

For example, let’s say a bakery hires a general contractor to install a new roof, and has its contractors list it as an additional insured. During construction, debris falls and injures a bakery employee. Out of work for six weeks, they sue the contractor, who, named as an additional insured, is covered by the subcontractor’s policy.

Claiming additional insured status presents several benefits to organizations, including the following:

- Responsibility: It places financial responsibility for a claim on the entity most likely to cause it.

- Loss History: It helps parties protect their loss history. If a claim occurs that’s the responsibility of a vendor, the additional insured wouldn’t have to assert the claim under its own policy—keeping its loss history low.

- Risk Mitigation: It holds entities responsible for potential risks.

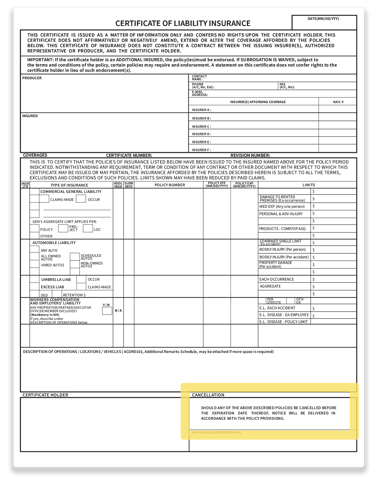

On an ACORD 25 certificate of insurance (COI) form, additional insured endorsements can be found in two places:

- The slim column labeled

“ADDL INSD” - The “Description of Operations” section at the bottom, providing a more detailed listing

To add an additional insured to a policy, contact your insurance provider to add their name and address.

Blanket Additional Insured Endorsements

If there are multiple third parties a business wishes to extend additional insured coverage to, they might use a blanket additional insured endorsement.

As the name suggests, blanket additional insured endorsements extend insurance coverage to multiple parties, without having to request additional insured status for each.

This option has some pros and cons:

Pros:

- Convenience: Blanket endorsements cover your bases, so to speak, without having to tediously request additional insured status for everyone.

- Reduces Coverage Gaps: Businesses might work with hundreds of vendors at a time, and missing vendor documents or inaccurate information may leave them without the coverage they need. Blanket endorsements reduce the likelihood of these mistakes—bypassing traditional steps to ensure all have coverage.

Cons:

- Ambiguous Language: Shared language about blanket endorsements haven’t been tested in court, creating some ambiguity around these documents.

- Completed Operations: Blanket endorsements also lack coverage for completed operations, which creates significant gaps for many projects.

- Notices of Cancellation: Securing notices of cancellation helps businesses limit risks, but doing so requires additional insureds to be listed on the policy. Blanket endorsements make this more challenging, as named insureds aren’t required to list additional insureds on them.

- Contracts Required: Blanket endorsement terms will usually depend on each policy. However, as most require a signed contract between two parties, it’s a good idea to keep these documents on hand to confirm additional insured status in a claim.

Ongoing vs. Completed Operations

Ongoing and completed operations coverage refers to how and when contractors can extend coverage for additional insureds.

- Ongoing operations endorsements provide coverage for jobs that are still in progress, or ongoing.

- Completed operations, however, come into effect after the work’s been finished.

Let’s take a look at an example.

![]() An office space is having some plumbing work done, and the contractor leaves his ladder in the hallway. An office employee walks into it, stumbles, and sprains her wrist.

An office space is having some plumbing work done, and the contractor leaves his ladder in the hallway. An office employee walks into it, stumbles, and sprains her wrist.

This is an example of bodily injury occurring during ongoing operations, while the contractor is working at the office space. But what happens if one of the pipes bursts weeks down the line because of a mistake the contractor made, and someone is injured then?

If the contractor had listed the office space as an additional insured for completed operations, they may have coverage under the contractor’s policy.

Common Additional Insured Endorsements

Not all additional insured endorsements are created equal.

Let’s review some of the most common of these, or Additional Insured-Owners, Lessees or Contractors endorsements:

- Scheduled Person or Organization (CG 20 10): This endorsement covers contractor liability for bodily injury, property damage, or personal and advertising injury that occurs during ongoing operations only. It only provides coverage for claims filed while a job is still in progress, or ongoing.

- Completed Operations (CG 20 37): As the name suggests, this covers claims occurring after the work’s already been finished, or completed operations.

- Automatic Status When Required in Construction Agreement With You (CG 20 33): This blanket endorsement is commonly used in the construction industry, covering parties you’ve agreed with in writing should be listed as an additional insured under your policy. Their additional insured status ends when you've completed operations for them.

- Automatic Status For Other Parties When Required in Written Construction Agreement (CG 20 38): Also commonly used in construction, this blanket endorsement covers upstream parties—those above the level a party is contracting—along with anyone else you’re contractually required to add.

Primary & Non-Contributory Endorsements

When multiple additional insureds are listed under an insurance policy, it can be difficult to know who should contribute to a claim first, and how much.

Primary and non-contributory endorsements clarify these questions.

- Primary endorsements specify the first party responsible for responding to a claim, before another party’s policy applies.

- Non-contributory endorsements prevent insurers from seeking contribution from other policies to cover the costs of a claim, and specify whether and which parties should contribute if a claim exceeds coverage limits.

![]() For instance, let’s say a museum hires a contractor to remodel its exterior. However, one subcontractor doesn’t properly secure the masonry stones, and some debris falls and injures a passerby’s foot. He sues the museum, contractor, and subcontractor.

For instance, let’s say a museum hires a contractor to remodel its exterior. However, one subcontractor doesn’t properly secure the masonry stones, and some debris falls and injures a passerby’s foot. He sues the museum, contractor, and subcontractor.

When the museum receives the claim, it passes it along to the contractor, who tenders it to the subcontractor. The subcontractor’s insurance responds first, and without seeking contribution from the policies of the museum or contractor. If the subcontractor’s limits are exhausted, the museum’s and contractor’s policies will respond within the terms of the contract requirements.

While this may seem similar to a waiver of subrogation, it’s fairly different. A waiver of subrogation prevents insurers from seeking contribution from negligent third parties to recoup amounts already paid toward a claim.

Waivers of Subrogation

Before we dive into waivers of subrogation, let’s first understand what subrogation is.

When an insurance company covers a claim, they have a legal right to pursue the party responsible to recoup costs—a right known as subrogation.

So, a waiver of subrogationwaives this right, meaning the insurer is prevented from pursuing a negligent party to recoup amounts paid toward a claim.

Let’s say Charlie Customer is shopping for a birthday gift in a local business, within a larger plaza. When he walks into the store, he doesn’t notice the carpet is torn, and trips and breaks a leg. This keeps him out of work for three months, so Charlie takes legal action against the shop, whose CGL policy compensates him.

Let’s say Charlie Customer is shopping for a birthday gift in a local business, within a larger plaza. When he walks into the store, he doesn’t notice the carpet is torn, and trips and breaks a leg. This keeps him out of work for three months, so Charlie takes legal action against the shop, whose CGL policy compensates him.

The plaza’s property manager was responsible for replacing the rug, but the shop had just signed a new lease that included a waiver of subrogation favoring the property manager. So, when Charlie’s insurance moves to collect payments from the property manager, it’s blocked by the waiver of subrogation.

Waivers of subrogation exist to contain financial losses to a specific party’s insurance policy. They protect third parties financially, help preserve business relationships, and avoid the need for lawsuits.

However, they also typically make insurance premiums more expensive, and it’s also important to read contracts thoroughly as to not accidentally breach it by neglecting any waiver-prohibiting language.

Waivers of subrogation can be found on a certificate of insurance (COI) in two areas:

- The “SUBR WVD” Column

- The “Description of Operations/Locations/ Vehicles”

How Waivers of Subrogation Help

While COIs prove valid insurance coverage, they don’t contain all the details of the policy. This means those interested in partnering with a vendor might not have a complete understanding of its coverage or any applicable exclusions.

Waivers of subrogation provide another level of protection. Without it, there may be gray areas in the event of a claim.

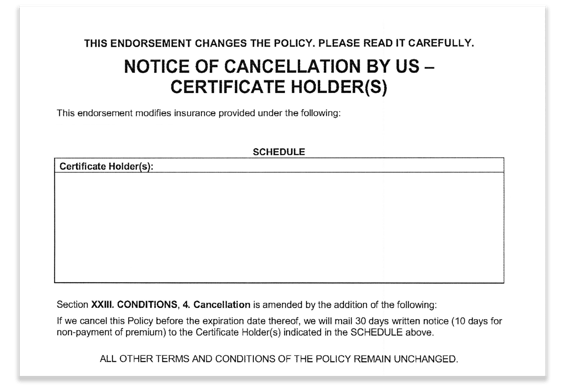

Notices of Cancellation

Have you ever gone out with someone, and they suddenly stop responding to you without any warning? Well, so-called “ghosting” can happen in the insurance world, too.

If vendors you are working with cancel their insurance policies and decide not to renew, this can leave your company exposed to risk. So, it’s important to obtain a notice of cancellation (NOC) from them notifying when vendors cancel their insurance policy or decide not to renew it.

Most policies come with a NOC, which can traditionally be found in the lower right corner of a COI.

These endorsements also outline the amount of time you have to cancel a policy without incurring penalties or fees. It’s important to be aware of this cancellation period, which varies depending on the policy but is usually 30 or 60 days. Keep track of these time frames and make any necessary changes to your insurance within them.

While they're essential for mitigating risk, notices of cancellation are not always guaranteed—potentially leaving parties unaware of pending cancellation.

Make it a priority to collect these endorsements from contractors by:

- Verifying relevant parties are included on the endorsement form, along with an address where the NOC should be mailed.

- Ensuring your insurance requirements include specific language requiring the vendor’s insurer to provide a NOC, non-renewal, or non-payment of premium.

- Including language that the vendor should give you a copy of the NOC providing the required notice.

- Obtaining a copy of the NOC to ensure its language provides the desired notice.