ACORD Changes & Vendor Risk Management

ACORD recently made several changes to their standard certificate of liability insurance form, currently one of the most widely used insurance certificates. This alteration poses several important risk management issues for companies that contract with suppliers and vendors.

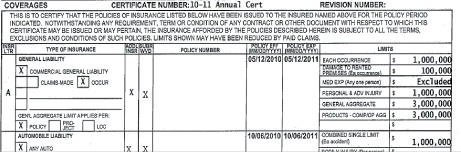

The most-discussed change to the ACORD 25 (2009/09) form is to the Cancellation provision; wherein specific language to provide notice to the Certificate Holder in the event of a policy cancellation had seemingly been removed.

The prior language on the ACORD 25 (2009/01) form read: “Should any of the above described policies be cancelled before the expiration date thereof, the issuing insurer will endeavor to mail _____ days written notice to the certificate holder…” In short, the above language stated that if any of the policies listed on the ACORD form were cancelled, the insurance provider would send notification to the affected certificate holder/s. The space was left blank so that an insured could have their insurance agent or broker write-in a number of days notice of cancellation.

The new language on the updated ACORD 25 (2009/09) was changed to read: “Should any of the above described policies be cancelled before the expiration date thereof, notice will be delivered in accordance with the policy provisions.” This new language caused much debate, because upon initial glance it seemed to remove the ability for the insured to specify how many days notice the Certificate Holder would receive in the event of policy cancellation.

In reality, the new ACORD form language reinforces that the language of the policy, not the certificate, is what matters. The point to consider is that the> protection offered by the earlier ACORD form cancellation language was largely illusory. In the earlier form, by stating that the insurer “will endeavor to mail” notice, and that “failure to do so shall impose no obligation or liability of any kind upon the insurer,” these caveats eroded the insurer’s or agent’s obligation to provide notice of cancellation. Even if an insurer indicated on a certificate that they would mail 30 days notice of cancellation, unless they were required to do so by the policy, they were likely under no obligation to actually provide that 30 days notice.

The new ACORD form cancellation language simply states what the previous form meant, namely, the cancellation notice will be mailed in accordance with what the actual policy requires, not based on what is written on the ACORD form. On the ACORD form it states: “This certificate is issued as a matter of information only and confers no rights upon the certificate holder.” In other words, the actual policy is what counts.

This change to the ACORD form has several implications. For example, many vendors have contract stipulations requiring them to provide a specific number of days cancellation on their policies. With the new ACORD form, it is less apparent or indicative of whether that protection is actually part of the policy. Certificate Holders have several options in light of the new ACORD form language.

These suggested actions include:

- Collect follow-up certificates of insurance on a quarterly basis, rather than on the insurance policy anniversary date. This allows for regular confirmation that the required insurance is still in force and the premium

has been paid up through the date the certificate was issued. - Ask the insured to modify their insurance policy by endorsing the required cancellation notice language. Then, collect a copy of the

cancellation notice endorsement along with the certificate. - Remove and / or modify the cancellation wording in the insurance section of vendor contracts.

- Collect a copy of the insured’s insurance policy and review the appropriate cancellation notice language directly, to see what the policy actually says, rather than relying on ambiguous certificate wording.

- Ask the insured to work with their insurance agent to provide cancellation notice to the Certificate Holder. Some insurance agents are beginning to see this as an additional service they can provide to their insureds, though it should be approached on a case-by-case basis, as insurance agent services and ability varies greatly.

As always, the main consideration is time and expertise. The new ACORD changes may or may not affect your company’s risk management strategy or vendor relations. This depends on what your current vendor requirements are, and whether your vendors actually follow these requirements. If your organization may be affected by this change, you need to have properly trained staff available to review vendor insurance certificates, to determine whether they are in compliance with terms and conditions after their insurance broker begins using the new ACORD forms.

Subscribe Now

Learn from the pros about risk-mitigation, document tracking, and more, with expert articles from bcs.